CLAIMS SUBSTANTIATION FOR PAYMENT OR REIMBURSEMENT OF MEDICAL AND DEPENDENT CARE EXPENSES

CLAIMS SUBSTANTIATION FOR PAYMENT OR REIMBURSEMENT OF MEDICAL AND DEPENDENT CARE EXPENSES

A memorandum released by the IRS Chief Counsel responds to a request for assistance regarding the reimbursement of medical and dependent care expenses. Addressed is whether reimbursements of medical expenses from a health flexible spending arrangement (FSA) provided in a cafeteria plan should be included in an employee’s gross income if the expenses are not properly substantiated. The conclusion is that if any expenses, including those below a certain threshold, are not substantiated, the reimbursements must be included in the employee’s gross income.

The second issue concerns the method of substantiation for expenses. The document examines different scenarios, such as self-certification, sampling of expenses, not requiring substantiation for small amounts, and not requiring substantiation for charges with favored providers. The conclusion is that if a cafeteria plan does not require proper substantiation, it fails to operate in accordance with the regulations and the benefits must be included in the employee’s gross income.

Read the full description of the scenarios, an analysis of the relevant laws and regulations on income tax withholding and the regulations for cafeteria plans and substantiation of expenses.

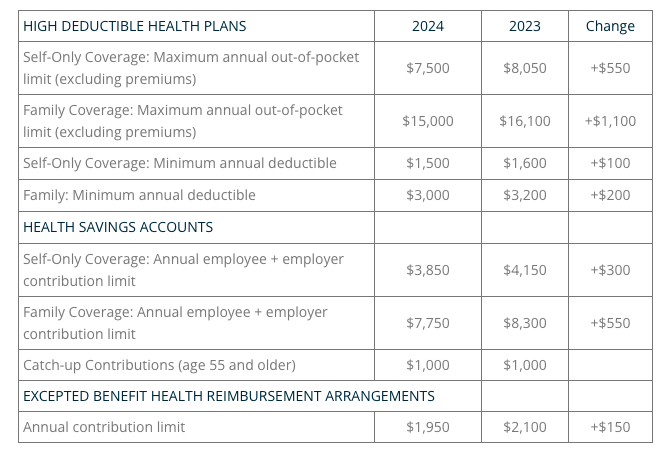

2024 LIMITS ANNOUNCED FOR HDHPS, HSAS, AND EXCEPTED BENEFIT HRAS

The Internal Revenue Service (IRS) announced the new limits for high-deductible health plans (HDHPs), health savings accounts (HSAs), and excepted benefit health reimbursement arrangements (EBHRAs).

The new limits for both HDHPs and HSAs will go into effect for calendar year 2024 while the HRA limits will go into effect for plan years beginning in 2024.

PREVENTIVE HEALTH SERVICES COVERAGE AND THE BRAIDWOOD DECISION

On May 15, 2023, the Fifth Circuit Court of Appeals temporarily halted the enforcement of a district court’s ruling in the Braidwood Management Inc. v. Becerra case. The district court had invalidated a portion of the Affordable Care Act (ACA) that required coverage of certain preventive care services without cost-sharing, citing religious beliefs as the reason for the violation. The Justice Department appealed the decision, and while the appeal is ongoing, the Fifth Circuit issued an administrative stay, effectively reinstating the ACA’s requirement for full coverage of preventive care. A final decision from the Fifth Circuit is expected later this year.

The Braidwood decision concluded that the determination of certain preventive care requirements under the ACA violated the Appointments Clause of the United States Constitution. These requirements are typically based on recommendations from entities such as the United States Preventive Services Task Force (USPSTF) and the Health Resources and Services Administration (HRSA). However, the court’s ruling specifically targeted recommendations made by the USPSTF after March 23, 2010.

The Departments of Labor, Health and Human Services, and the Treasury, responsible for enforcing the preventive service coverage requirements, have appealed the court’s decision. The Departments have issued an FAQ clarifying the impact of the Braidwood ruling, stating that it only applies to services recommended by the USPSTF after March 23, 2010, and does not affect guidance related to immunizations recommended by the Advisory Committee on Immunization Practices (ACIP) or comprehensive guidance supported by the HRSA. State laws may still require coverage of USPSTF-recommended services.

Although the Braidwood decision suspends the enforcement of certain preventive care coverage, it is expected that few employers will make significant changes until the outcome of the case is determined through the appeals process.

QUESTION OF THE MONTH

Q: Throughout the pandemic, our company’s group health plan has covered COVID-19 testing and vaccines at no cost to plan participants. Is this still required now that the public health emergency has ended?

A: During the COVID-19 public health emergency (PHE), group health plans had to cover COVID-19 testing and vaccines without cost-sharing or restrictions. Coverage requirements for diagnostic testing no longer apply after the PHE, but plans are encouraged to continue providing coverage at no cost. However, plans may choose not to cover tests or impose cost-sharing. The requirement to cover COVID-19 vaccines as a preventive service remains in effect for non-grandfathered health plans, but coverage for out-of-network providers is no longer mandatory if there is an in-network option. Plans are encouraged to notify participants of any changes to COVID-related coverage, and modifications must be disclosed at least 60 days in advance, except for changes that revert to pre-PHE conditions.

© UBA. All rights reserved.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

Top

Top